In case you have been living under a rock the past week, there is a chance you may not have heard about the crisis in Greece. They are bordering on a full economic collapse.

This isn't the first time Greece has flirted with economic problems. U.S. investors have limited their dealings with the country after it endured two previous bailouts; now Greece is flirting with it's third. Economist Ted Loch-Temzelides, according to ABC News, doesn't expected our economy to suffer as a result because they are not a major exporter to the US. There was drop in U.S. stocks and a prediction that some hedge funds will suffer, but that's it.

But why is Greece in this mess? What did they do?

ABC News reports that the crisis escalated when the Syriza party came into power after the January elections, but that's only the very infinitesimal tip of the iceberg. The real issues started before that.

After the implosion of Wall Street in 2008, Greece found itself in the center of the European debt crisis. Greece revealed in 2009, that they "had been understating its deficit figures for years," according to the New York Times. With a massive amount tax evasion within the nation, it is no surprise that debt is the culprit. Even though Greece has received two bailouts, the money essentially went back to the lenders instead of providing another start for the economy. They, literally, have no money to pay back anything.

The country went to the polls Sunday on whether or not to accept a bailout from the German and French banks. Surprisingly, the country voted no with an overwhelming 61.07 percent. It was cited that the heavy austerity reforms were a driving force. The lending agencies wanted the Greek government to cut pensions by one percent of the national GDP, but Greece was only willing to do half of that. There was also talk of raising taxes (and actually collecting them), and also a cut back on social security.

The Washington Post reports that unemployment in Greece is worse than unemployment in the U.S. was during the Great Depression.

As of right now, banks in Greece are closed to avoid running out of cash. So far, ATM withdrawals are limited to roughly 60 euros a day because tens of billions of euros were removed after the fear of an economic collapse. With negotiations still on hold, and no end in sight, the people of Greece are stuck. While 60 euros (roughly $66) per day may seem like a lot, consider the fact that bills must be paid and families must be fed. For those who live on islands, access has been extremely limited.

There is now speculation that Greece may abandon the euro and switch over to drachmas in a move being called the "Grexit" (Greek exit), or they could even be kicked out of the Eurozone. Greece is still holding onto the idea of easier bailout terms and less debt, but it still in up in the air whether the other countries will agree to the these terms.

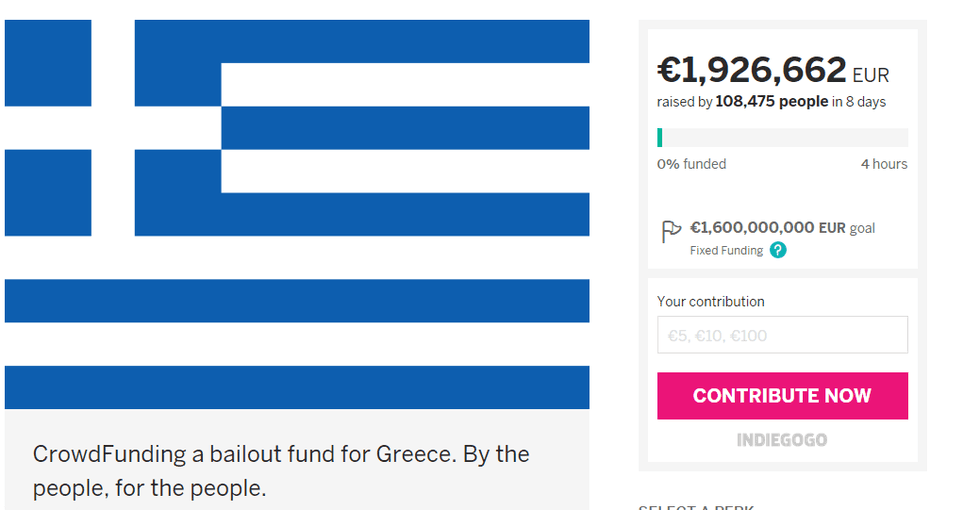

Hopefully, Tuesday will bear some fruit and Europe will be one step closer to fixing this crisis. In the mean time, a young man from Yorkshire, named Thom Feeney, is determined to help.

Fed up with the current situation, he started an IndieGoGo fund to help raise money through crowd funding. So far, almost 2 millions euros have been raised in a little over a week. This campaign has found a strong foothold on social media. If you wish to donate, you may do so here: https://www.indiegogo.com/projects/greek-bailout-fund#/story.

Were is the U.S. in this situation? Would we, as a nation, put aside our petty differences to come to Greece's aid? Hopefully, stubbornness will not win and Greece with find a resolution. If they don't come to an agreement soon, Greece will suffer a total economic collapse; it will just be a matter of time.