In August 2015, the Shanghai Stock Exchange experienced its worst crash in almost a decade. Trillions were eviscerated, which caused a massive drop in value for some of the richest investors and companies in China and sent shock waves around the world. In the final weeks of December 2015, the United States Federal Reserve (the central bank of the US) announced its first interest rate hike in seven years on the basis of an improving American economy. In the first week of January 2016, the Chinese stock market crashed once again, causing the worst opening of international stock markets in a new year ever recorded. These events tell a story of an international economy that is intertwined for good and bad; it is a product wrought by globalization.

That dragon looks scared

That dragon looks scared

The Chinese economy has been slowing down for quite some time, and most likely will continue to decelerate. For over two decades, China achieved stellar, double-digit growth rates. This led to the rise of hundreds of millions from poverty and the development of specific sectors of China’s economy. It also created a dismal situation for workers’ rights, produced grotesque pollution, and exacerbated inequality, particularly between coastal areas and impoverished inland regions. For almost 20 years, China was the engine of economic growth for the world, proving to be a bulwark even during the global recession of 2008. This dynamic, however, is changing. The Chinese economy is slowing down. Growth rates that used to hit double digits are now struggling to hit 7 percent for 2015.

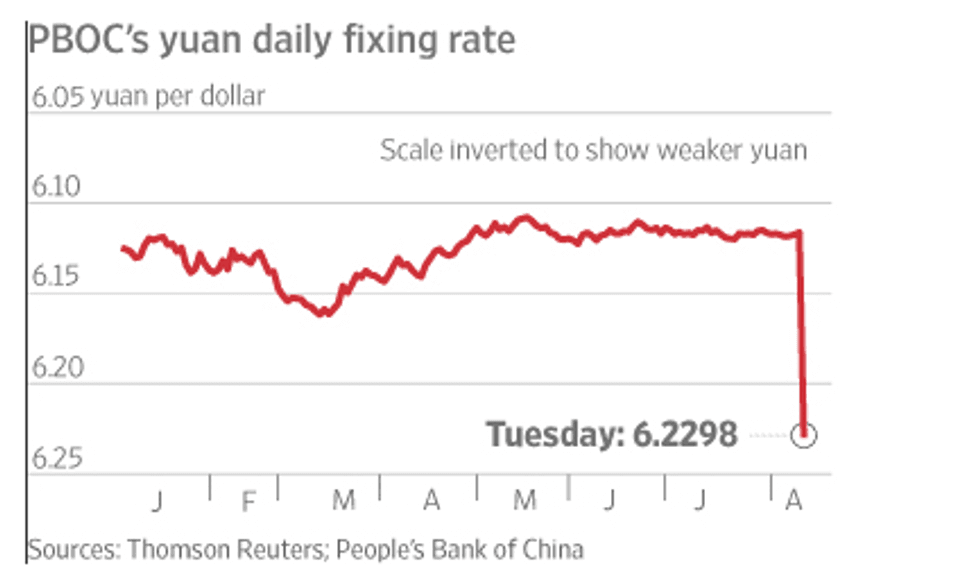

The primary concern is the slowing growth of Chinese exports that supply the world with cheap consumer goods. To combat this, the central bank of China, which is an inherently political institution of the Communist Party, intervened by devaluing the Chinese yuan against the American dollar. By lowering the value of the yuan (also called the renminbi), Chinese exports are made more competitive against exports of other countries with higher value currencies, thereby making Chinese goods more compelling for consumers abroad. In other words, devaluation makes Chinese-made goods cheaper. That makes their goods more competitive for consumers abroad. This devaluation, however, defies the international standard of letting financial markets freely determine the value of another country’s currency. It also panicked investors by explicitly letting them know that the Chinese economy is in trouble.

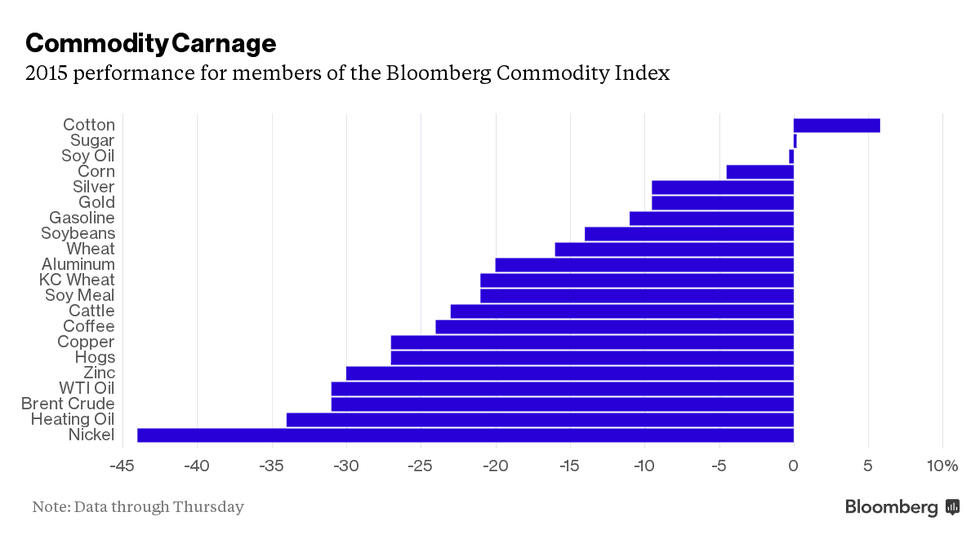

The People’s Bank of China (PBOC) devalued the yuan against the dollar twice in August and once again in January. The devaluations were tactical moves by the PBOC to allay the exports problem, but they alarmed investors, which caused massive sell-offs around the world and two stock market crashes. They also introduce problems of their own. Commodities all over the world are denominated in dollars. Raw materials like minerals, gold, copper, oil, and metals are usually priced in dollars regardless of whether an American is involved in the transaction. This is considered normal. If financial markets change the valuation of the dollar, it only marginally affects the buyers and sellers of other countries (supply and demand move around because reasons). However, if a government artificially lowers the value of its own currency, it winds up paying more for commodities. China has become a massive consumer of commodities, much of which comes from Africa, to power its economic growth. Of course, as overall economic growth slows, the demand for such commodities will also slow, but what it does buy may be more expensive because of the devaluation.

Almost all commodities are down, especially oil. If China consumes fewer raw materials, this chart may go even further left

The intervention of the PBOC is also behavior unwelcome by the international community. As of this month, October 2016, the yuan is part of the Special Drawing Rights (SDR), a basket of foreign currencies designated by the International Monetary Fund. This basket is composed of currencies that are used by countries and corporations everywhere when making transactions and are the forms in which most wealth is stored. It includes the US dollar, the British pound, the Japanese yen, the Euro, and (soon) the Chinese yuan, which means these are the most prolific currencies. Any time a corporation makes a transaction, or a government makes a payment, or a donation is made to an international aid agency, there is a good chance that it is done in one of these currencies. One of the conditions for entrance into the SDR is transparency in monetary policy and allowing financial markets to determine currency valuation. The Communist Party has maintained an iron grip on the value of the yuan for years in order to bolster exports, which many criticize as an illegal trading practice. As the yuan joins the SDR, though, the Communist Party will supposedly relinquish control and eventually cease intervention. Interestingly, the recent devaluations are not contradictory to this statement: many experts believe the real worth of the yuan is actually lower than it is now. The Communist Party may have artificially set the bar, but it is still closer to where it should be now compared to before. What is contradictory is the intervention itself. China will not release full control yet because it could lead the economy even more downward, but it should soon.

The valuation of the yuan compared to the dollar. It dropped by about 0.3 in one day. And yes, that freaks people out...

The stock market crash has social ramifications too. The current slowdown will likely not recede. One way the Communist Party has dealt with it is by making a scapegoat of some of the wealthiest citizens of China. In recent months, hedge fund managers, CEOs, and other successful people have been detained and interrogated for a variety of crimes, including falsifying financial reports. While it’s reasonable to believe that at least some corruption exists, it is bad for business to detain prominent individuals for political reasons. For all the bad they may have done, these men and women have in fact provided much of the economic growth of China. If standards of integrity are to be used, they must be upheld at all times, not just when the Communist Party wants to pin blame on someone.

Stock market crashes also worry ordinary Chinese citizens. In order for China to develop into an economically stable market, personal consumption must increase. China cannot continue to be a low-end manufacturer, producing toys and shirts for the world. It needs to evolve into a higher-end manufacturer. Consumer spending also needs to increase to sustain economic growth, like how consumer spending in the US sustains the American economy. The financial services industry also needs to continue growing as well. This will ensure continued growth of the economy while slowing the growth of debt. The rise in interest rates by the US Federal Reserve may help in this regard.

For over seven years, the Fed has kept interest rates in the US at a bare minimum. This kind of monetary policy encourages greater borrowing from banks. Individuals looking to buy a home and companies looking to engage in new investments have benefited from low-interest rates, causing a flood of cash to enter various markets. By encouraging borrowing, the Fed hoped to improve the American economy. This strategy, called quantitative easing, worked to an extent. This generated some of the economic growth since the recession, even as meager as that growth has been. Much of this money found its way to the developing world, which in turn financed a lot of economic growth abroad. Firms in China, for example, were able to attain American money to expand, but they also accrued significant debt.

Being in debt, whether on a micro or macro scale, is not necessarily a bad thing. Individuals take out loans to acquire material possessions or start businesses. Companies take out loans to start new projects or expand. So long as a steady stream of income ensures that payments are made to pay back loans and interest, being in debt is not bad. In fact, it’s actually good, because it means that an economy is active. If a person were never to take out a loan, it would be difficult to buy a car or a home. If a company were to never take out a loan, it would be difficult to grow a business. These things are bad for the economy overall. It’s also bad for the creditor and debtor if a loan is taken out but not repaid with interest. Loans, much like everything else, have silver linings.

On a micro scale, individuals can set their own silver linings. On a macro scale, it is typically bad for countries to have a debt-to-GDP ratio larger than 100%. GDP is analogous to measuring how much a country is worth, in a monetary sense; a ratio larger than 100% is like saying that a country owes more than it is worth. China is a corrupt one-party state where official facts and figures are dubious at best. Unofficial studies, conducted outside the Communist Party, estimate that the debt-to-GDP ratio is almost 200%. Much of that debt was accrued during the era of cheap American money. That era is not yet quite over, since the Fed only increased interest rates by a bit (~0.25%), but it should discourage borrowing. As the economy slows, corporate revenue takes a hit and a company becomes hard-pressed in repaying its loans. If the debt-to-GDP ratio is in fact 200%, China may be in a credit bubble of giant proportions. The government can’t help every company, which means that many will go bankrupt. What remains to be seen is how bad of an impact this will produce for China and the rest of the world. What will happen when this bubble pops?

The global economy will likely go into panic mode, as it did in August and January, although the degree of that panic may be far worse. It could be as bad as it was in 2008, when the US thrust the entire world into recession. This time, however, the US is in much better shape now than it was before. The unemployment rate is below 5%, there are many realms of advanced technology that promise economic expansion, and wages are finally increasing, although just barely. Perhaps one of our biggest dilemmas is the extreme partisanship in Washington DC. The presidential election has also been bat shit crazy so don’t discount that. Still, we are in much better shape than we were in 2008 and could potentially weather an economic storm wrought by China. Who that storm will affect the most, though, is the European Union, which is China’s biggest trading partner. Various commodities suppliers, mostly in Africa and Central Asia, will also hurt as demand slows in China.

If the Chinese credit bubble does pop, then the volatility could be far more encompassing than the current market turmoil. The present situation is confined to the global stock market, which is always a lot more volatile and unstable than other economic sectors. As an old adage goes, “the stock market has predicted nine of the last five recessions.” Financial markets are unreliable as fortunetellers and investors have a tendency to overreact. Moreover, China is in fact doing many of the things that it needs to do to transition: consumer spending is increasing, borrowing is going down, and the Communist Party is (slowly) releasing control of the yuan. But the era of high Chinese economic growth is likely over. It will take time for people to get used to that.

One final note: this is all a result of a more connected world. Why is it that what happens in one country affects things everywhere else? How can some numbers and charts that don’t move the way people expect make everyone panic? It seems quite absurd when you take a step back, but that is what happens when a global economy joins to the hip. It is a result of globalization, a glorious process that connects us all and makes our world perceptibly smaller, for good and bad.