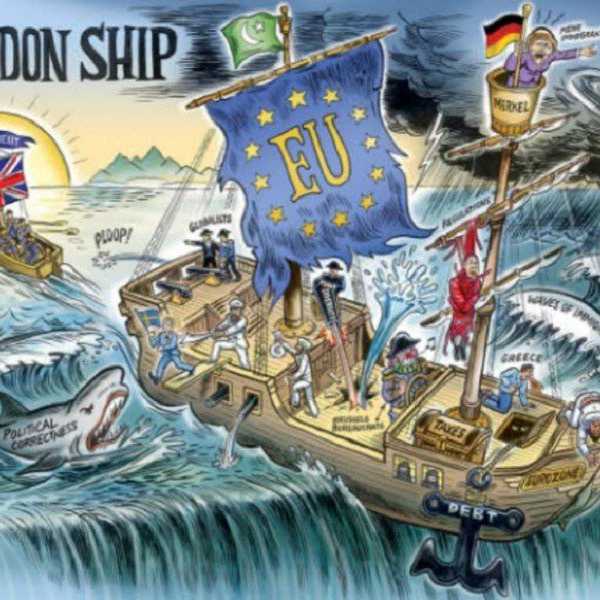

Buckle up, folks, it’s time to talk some geopolitical economics. Let’s start with a quick history of the European Union (EU) and the Eurozone. The EU was formed in early 1993, and consists of a complex system of political and economic interdependency between twenty-eight European nations. The Eurozone is a subset of that union, established in 1999, wherein nineteen of those member states share a single currency – the euro. What this means is that individual countries do not print their own money, but rather collaborate to establish unified monetary policy and lay the groundwork for an international economy. This monetary union – one of the largest of its kind – has been hailed as a bold step towards further uniting a continent that has all too often been divided. Though not without its critics and crises, the Eurozone seemed to be functioning smoothly.

Then 2010, and its accompanying global financial meltdown rolled around. That’s when things started to go a little sideways for the Euro. The causes of this crisis were many and varied, but the end result was that virtually all markets in the U.S. and Europe were nailed with the worst shock this side of the Great Depression. Some countries, such as Germany and England (the latter, incidentally, being a member of the EU but retaining currency independence with the Pound Sterling), were able to weather the storm more or less intact. Others have had a harder time getting back on their feet. None more so than Greece.

The exact cause of Greece’s economic woes is up for debate, but the results are only too plain to observe. Crippling debt, skyrocketing unemployment, a lack of essential industries; there are few economic blows that Greece hasn’t taken squarely to the chin. Needing help to keep their economy afloat, Greece was forced to turn to international sources for aid. Stronger Eurozone economies, afraid of what would happen should the Euro collapse in one country, were virtually forced to bailout the Greek economy. Of course, they did not do this for free – each loan was coupled with increasingly stringent conditions.

And so it went for several years. Greece would dig itself into a deeper hole of debt and request aid, Germany and other Eurozone leaders would threaten harsher austerity measures, but the loan would ultimately go through somehow and the cycle would start anew. Unsurprisingly, the Greek people soon grew fed up with this state of affairs. This provided the opening for the far-left Syriza party – running on promises of change and standing up to the Eurozone – to seize control of parliament in the national elections. Upon taking office, Prime Minister Alexis Tsipras was able to alleviate the concerns of both the Greek people by promising to forge a middle way, one that would lift Greece out of economic disarray while also maintaining her status in the Eurozone.

Over the past few months however, things haven’t been going too great for Greece. Greek citizens have been restricted to withdrawing no more than sixty euros a day from their bank – the equivalent of just under seventy U.S. dollars. The national debt has not gotten any smaller. Tsipras has had difficulty seeing eye-to-eye with other European leaders when it comes to what strings should be attached to loans. Things seemed to come to a head this past week when Greek voters – at the urging of Tsipras’ government – overwhelmingly rejected the latest batch of austerity measures in a nationwide referendum. Riding high, Tsipras returned to the negotiating table firm in the knowledge that his people trusted him to fight for a new deal. After a few days, he returned with a fresh proposal in hand.

A proposal that, aside from a few technical details, was by-and-large the exact same deal that Greek voters had just rejected. Included in the austerity measures are such things as increased taxes, drastic cuts in spending and harsher restrictions on repayment. The Greek people, quite understandably, felt betrayed and demanded Tsipras work for a better deal. Unfortunately for Greece, resentment has been growing among fellow Eurozone members. Countries such as Finland have been hesitant or have outright refused to loan the roughly eighty billion Euros requested, and Germany has even gone so far as to call for Greece’s temporary removal from the Eurozone.

Talks are still up in the air. No one is exactly sure what will happen for Greece, but there have been growing calls for the nation to finally leave the Eurozone. However, there is no real formal policy for withdrawal or expulsion from the monetary union, and economists are unsure what such a withdrawal would mean for both Greece’s flailing economy and for the Eurozone as a whole. Would such a withdrawal prompt other struggling countries – Spain and Italy come to mind – to flee the union as well? Would the very foundations of the Eurozone be shaken and called into question? Better students of the economy than me are unsure, so I won’t dare speculate much. The only thing that can be known is that the coming weeks in Europe will be well-worth paying attention to.