Economics are not an exact science, but economists love to tell you it is.

Economics and "the economy" has been one of the biggest buzzwords I've heard in recent memory. We rely so heavily on this day today, yet so many people know almost nothing about it. If you hear the words macroeconomics and microeconomics, and scratch your head in confusion- you've arrived at the right article! I study financial economics, and I'm also minoring in economics, so I am supposed to be an expert in the field by the time I graduate- so welcome to the first volume of a series of economics web-based learning which will be a learning experience for me, and you, the reader. First and foremost I want to say that when it comes to economics there are so many variables that if you were to make a function out of it you would have an exponentially large polynomial -- it is so important to know that economics are based on theories and you use information, data, and statistics to find trends which will tell you where you are going by looking at where you've been. Please bear in mind that when it comes to economics, there is a lot to cover, so this is the first entry of many that will go in depth into what makes the economy what it is. I like to think of the economy as an ocean with its own tide. Products, goods, services, costs, all of these are waves in that ocean, and we are just riding the current along where it goes. What does the word economics mean? Economics refers to the branch of knowledge concerned with the production, consumption, and transfer of wealth. In other words, anything to do money, production of products or services, usage of said services/goods, and the transfer of wealth that occurs when those products/services/goods are transferred from one party to another.

Here are some lessons economics taught me over the years:

-Everything has a price, a cost, and even if it is "free" someone is still paying for it.

-Money is not the only thing we exchange for goods and services.

-Everything revolves around:

Supply and Demand:

We can break down one of the primary parts of the economy as the supply and demand. What we will look at first is why these two are always paired together. Generally speaking supply is how much of a product or service you have available. Demand refers to how much people want what you have. For example, during the 1800s to about the 1930s, the US was primarily a goods and industrial based nation, and around the end of that period, the US moved itself into a services based economic power. What that means is that no longer does the US infrastructure provide it's own goods and raw materials and thus imports much of its goods from countries like China. Therefore, the US's Supply switched from a priority of goods to a priority of services.

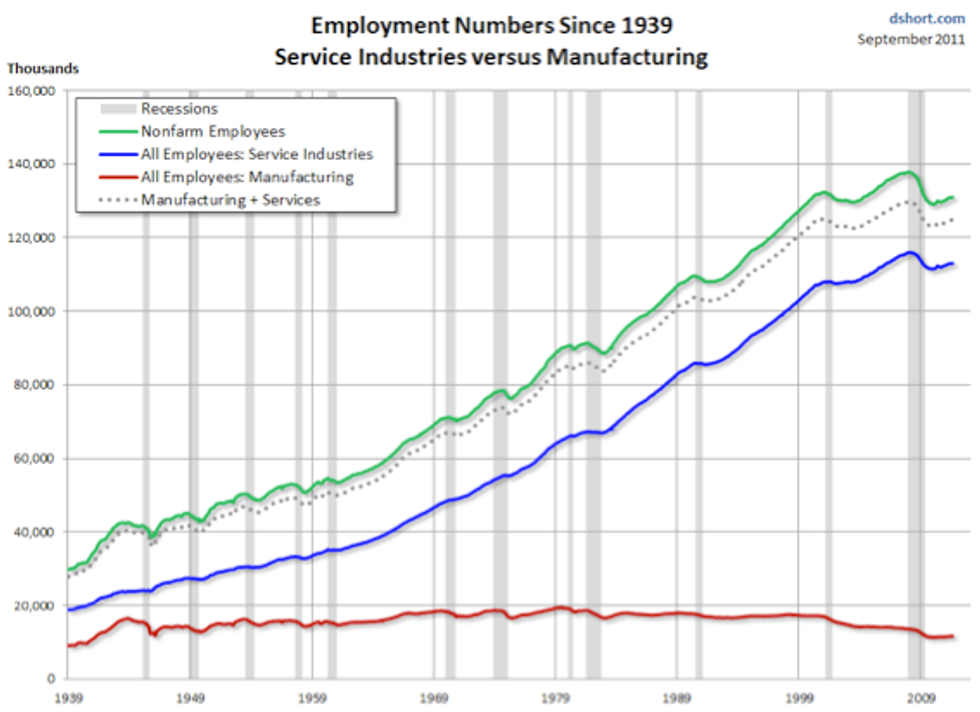

(graph from dshort.com)

The rubber band effect of economics, AKA Market Elasticity.

To see what I'm talking about graphically/visually, I have included this graph. The red line represents manufacturing of materials based on employment, and the blue, and green line. As you can see, Manufacturing is steadily trending downwards. Now you might ask, what does employment have to do with economics? Well, statistical figures in employment and industry play a big role in economics. Say there is a large demand for a material such as denim, and the US happens to have a very suitable means of production for it. Jobs will rise alongside the demand for denim, if the demand is large enough it will create jobs in denim factories and we can track this trend through supply and demand. We must supply enough denim, to meet or exceed the demand, if we don't, then prices will go up and denim will get more expensive, however, eventually there will be a point where one of three things will happen- 1 we will meet the demand and prices will intersect with supply and demand. This is called the Market Equilibrium. 2 we will fail to produce enough denim to meet the demand, and prices will increase because there simply isn't enough to go around. And lastly, 3 we will produce way too much denim, and the prices will fall because there is a surplus of denim. Congratulations, you've just learned Market Elasticity. Elasticity = (% change in quantity / % change in price.)

Moving forward, it's again imperative to know that these are merely guidelines behind what economics is about. Economics is a ever-present force that rules our lives from the clothes we wear, down to the food we eat, and where we live. It is the force that drives the most important thing, value. Without value for things, nothing would have any meaning. Economics impacts you in so many ways. I love seeing what exactly makes these things turn- and in that sense you now have learned the very basics to start actually learning about economics.